Does IRS Monitoring Matter for the Cost of Bank Loans?

IF 2

4区 经济学

Q3 BUSINESS, FINANCE

引用次数: 0

Abstract

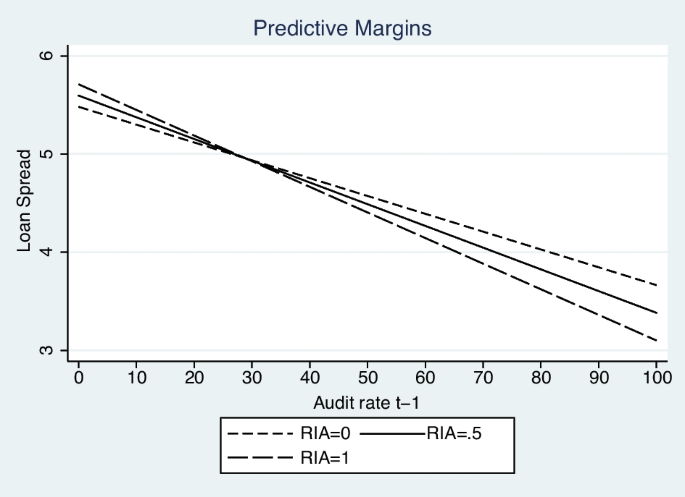

Abstract We show that IRS monitoring exerts a significantly negative effect on the cost of syndicated loans. A one standard deviation increase in the probability of an IRS audit decreases loan spreads by around nine basis points. We also find that this effect is stronger for borrowers with better lending relationships and credible access to public markets. These results indicate that IRS monitoring could increase the bargaining power of borrowers and restrain banks from extracting informational rents from their lending relationships. Thus, they provide a novel insight into how IRS monitoring could lower the cost of financing from the banking system.

美国国税局对银行贷款成本的监控重要吗?

摘要本文表明,IRS监控对银团贷款成本有显著的负向影响。美国国税局审计的概率每增加一个标准差,贷款息差就会减少约9个基点。我们还发现,对于借贷关系较好、能够可靠地进入公开市场的借款人,这种影响更大。这些结果表明,IRS监测可以提高借款人的议价能力,并限制银行从其贷款关系中提取信息租金。因此,他们为IRS监控如何降低银行系统融资成本提供了新颖的见解。

本文章由计算机程序翻译,如有差异,请以英文原文为准。

求助全文

约1分钟内获得全文

求助全文

来源期刊

Journal of Financial Services Research

BUSINESS, FINANCE-

CiteScore

3.00

自引率

7.10%

发文量

22

期刊介绍:

The Journal of Financial Services Research publishes high quality empirical and theoretical research on the demand, supply, regulation, and pricing of financial services. Financial services are broadly defined to include banking, risk management, capital markets, mutual funds, insurance, venture capital, consumer and corporate finance, and the technologies used to produce, distribute, and regulate these services. Macro-financial policy issues, including comparative financial systems, the globalization of financial services, and the impact of these phenomena on economic growth and financial stability, are also within the JFSR’s scope of interest. The Journal seeks to promote research that enriches the profession’s understanding of financial services industries, to elevate industry and product efficiencies, as well as to inform the debate and promote the formulation of sound public policies. Officially cited as: J Financ Serv Res

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: