Deep learning models for price forecasting of financial time series: A review of recent advancements: 2020–2022

引用次数: 0

Abstract

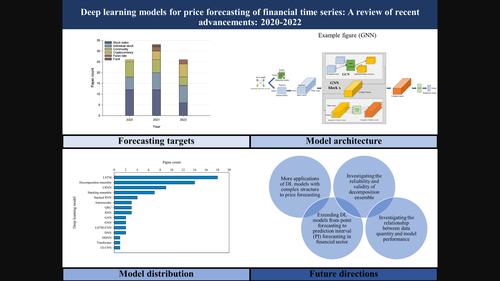

Abstract Accurately predicting the prices of financial time series is essential and challenging for the financial sector. Owing to recent advancements in deep learning techniques, deep learning models are gradually replacing traditional statistical and machine learning models as the first choice for price forecasting tasks. This shift in model selection has led to a notable rise in research related to applying deep learning models to price forecasting, resulting in a rapid accumulation of new knowledge. Therefore, we conducted a literature review of relevant studies over the past 3 years with a view to aiding researchers and practitioners in the field. This review delves deeply into deep learning‐based forecasting models, presenting information on model architectures, practical applications, and their respective advantages and disadvantages. In particular, detailed information is provided on advanced models for price forecasting, such as Transformers, generative adversarial networks (GANs), graph neural networks (GNNs), and deep quantum neural networks (DQNNs). The present contribution also includes potential directions for future research, such as examining the effectiveness of deep learning models with complex structures for price forecasting, extending from point prediction to interval prediction using deep learning models, scrutinizing the reliability and validity of decomposition ensembles, and exploring the influence of data volume on model performance. This article is categorized under: Technologies > Prediction Technologies > Artificial Intelligence

金融时间序列价格预测的深度学习模型:最新进展综述:2020-2022

摘要准确预测金融时间序列的价格对金融部门来说是必不可少的,也是具有挑战性的。由于深度学习技术的进步,深度学习模型正逐渐取代传统的统计和机器学习模型,成为价格预测任务的首选。模型选择的这种转变导致了与将深度学习模型应用于价格预测相关的研究的显著增加,从而导致新知识的快速积累。因此,我们对近3年来的相关研究进行了文献综述,以期对该领域的研究人员和从业人员有所帮助。本文深入探讨了基于深度学习的预测模型,介绍了模型架构、实际应用及其各自的优缺点。特别是,提供了关于价格预测的高级模型的详细信息,例如变压器,生成对抗网络(gan),图神经网络(gnn)和深度量子神经网络(dqnn)。目前的贡献还包括未来研究的潜在方向,例如检查具有复杂结构的深度学习模型用于价格预测的有效性,使用深度学习模型从点预测扩展到区间预测,仔细检查分解集合的可靠性和有效性,以及探索数据量对模型性能的影响。本文分类如下:技术>预测技术;人工智能

本文章由计算机程序翻译,如有差异,请以英文原文为准。

求助全文

约1分钟内获得全文

求助全文

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: