Haifeng Guo, Chi-Hsiou D. Hung, Alexandros Kontonikas, Yeqin Zeng

{"title":"Flight to Lottery Ahead of FOMC Announcements: Institutional Investors or Retail Investors?","authors":"Haifeng Guo, Chi-Hsiou D. Hung, Alexandros Kontonikas, Yeqin Zeng","doi":"10.1111/1467-8551.12755","DOIUrl":null,"url":null,"abstract":"<p>This paper studies the pre-Federal Open Market Committee (FOMC) announcement drift at the stock level. We hypothesize that investors have a higher propensity to speculate before the monetary policy announcements by the FOMC, due to the resolution of uncertainty and associated reduction in investors' fear. Indeed, we find evidence that there exists a drift of lottery-like stocks in the pre-FOMC window, when investors' fear gauge is lower, together with higher demand for lottery-like stocks and higher realized skewness. Moreover, we show that the demand for lottery-like stocks ahead of FOMC announcements is more prominent among institutional investors than retail investors. Our findings also identify the key role of transient and quasi-index institutional investors in our documented flight-to-lottery effect. Our findings advance the ongoing debates about the role of firms' investor heterogeneity in determining how monetary policy affects corporate managers' decisions. Our paper has important implications for central banks and managers by showing that investors' preference for lottery-like stocks increases before FOMC announcements.</p>","PeriodicalId":48342,"journal":{"name":"British Journal of Management","volume":"35 2","pages":"1076-1096"},"PeriodicalIF":4.5000,"publicationDate":"2023-07-31","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1467-8551.12755","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"British Journal of Management","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1467-8551.12755","RegionNum":2,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS","Score":null,"Total":0}

引用次数: 0

Abstract

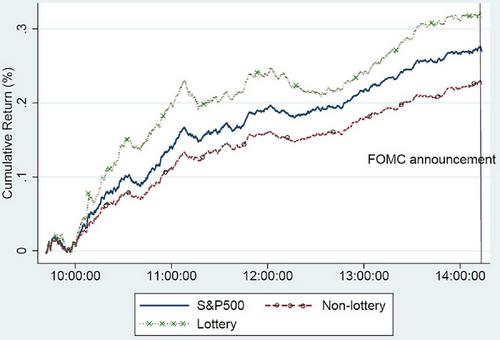

This paper studies the pre-Federal Open Market Committee (FOMC) announcement drift at the stock level. We hypothesize that investors have a higher propensity to speculate before the monetary policy announcements by the FOMC, due to the resolution of uncertainty and associated reduction in investors' fear. Indeed, we find evidence that there exists a drift of lottery-like stocks in the pre-FOMC window, when investors' fear gauge is lower, together with higher demand for lottery-like stocks and higher realized skewness. Moreover, we show that the demand for lottery-like stocks ahead of FOMC announcements is more prominent among institutional investors than retail investors. Our findings also identify the key role of transient and quasi-index institutional investors in our documented flight-to-lottery effect. Our findings advance the ongoing debates about the role of firms' investor heterogeneity in determining how monetary policy affects corporate managers' decisions. Our paper has important implications for central banks and managers by showing that investors' preference for lottery-like stocks increases before FOMC announcements.

期刊介绍:

The British Journal of Management provides a valuable outlet for research and scholarship on management-orientated themes and topics. It publishes articles of a multi-disciplinary and interdisciplinary nature as well as empirical research from within traditional disciplines and managerial functions. With contributions from around the globe, the journal includes articles across the full range of business and management disciplines. A subscription to British Journal of Management includes International Journal of Management Reviews, also published on behalf of the British Academy of Management.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: