Bayesian joint quantile autoregression

引用次数: 0

Abstract

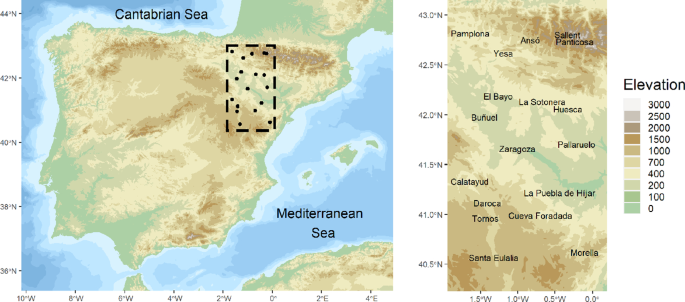

Abstract Quantile regression continues to increase in usage, providing a useful alternative to customary mean regression. Primary implementation takes the form of so-called multiple quantile regression, creating a separate regression for each quantile of interest. However, recently, advances have been made in joint quantile regression, supplying a quantile function which avoids crossing of the regression across quantiles. Here, we turn to quantile autoregression (QAR), offering a fully Bayesian version. We extend the initial quantile regression work of Koenker and Xiao (J Am Stat Assoc 101(475):980–990, 2006. https://doi.org/10.1198/016214506000000672 ) in the spirit of Tokdar and Kadane (Bayesian Anal 7(1):51–72, 2012. https://doi.org/10.1214/12-BA702 ). We offer a directly interpretable parametric model specification for QAR. Further, we offer a pth-order QAR(p) version, a multivariate QAR(1) version, and a spatial QAR(1) version. We illustrate with simulation as well as a temperature dataset collected in Aragón, Spain.

贝叶斯联合分位数自回归

分位数回归的使用不断增加,为习惯均值回归提供了一种有用的替代方法。主要实现采用所谓的多分位数回归的形式,为每个感兴趣的分位数创建单独的回归。然而,最近在联合分位数回归方面取得了进展,提供了一个分位数函数,避免了回归在分位数之间的交叉。在这里,我们转向分位数自回归(QAR),提供一个完整的贝叶斯版本。我们扩展了Koenker和Xiao的初始分位数回归工作[J] .中国生物医学工程学报,31(4):980-990,2006。https://doi.org/10.1198/016214506000000672)以Tokdar和Kadane的精神(贝叶斯分析7(1):51-72,2012。https://doi.org/10.1214/12-BA702)。我们为QAR提供了一个可直接解释的参数化模型规范。此外,我们还提供了一个p阶QAR(p)版本、一个多元QAR(1)版本和一个空间QAR(1)版本。我们用模拟以及在西班牙Aragón收集的温度数据集来说明。

本文章由计算机程序翻译,如有差异,请以英文原文为准。

求助全文

约1分钟内获得全文

求助全文

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: