Does e-commerce ease or intensify tax competition? Destination principle versus origin principle

IF 1.4

4区 经济学

Q3 ECONOMICS

引用次数: 1

Abstract

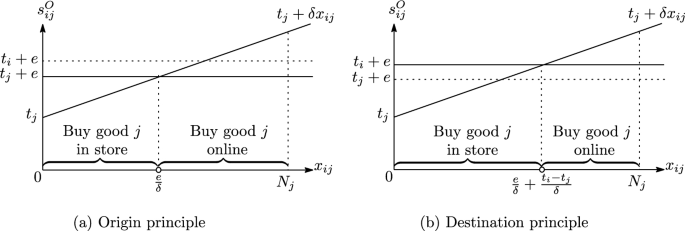

Abstract This study examines the relationship between e-commerce development and the intensity of commodity tax competition under two tax principles for goods purchased online: the destination principle and the origin principle. The main findings are as follows: Given that origin-based tax is applied to purchases made in brick-and-mortar stores, (i) tax competition under destination-based taxation on e-commerce is more intense than tax competition under origin-based taxation; and (ii) the expansion of the online market intensifies destination-based tax competition while easing origin-based tax competition. The main factor leading to the results is that replacing the choice of “where to purchase” goods, consumers will have a new choice of “how to purchase” when online purchasing becomes available, and destination-based taxation distorts the latter choice, while origin-based taxation is neutral.

电子商务是缓解还是加剧了税收竞争?目的原则与起源原则

摘要本研究在目的地原则和原产地原则下,考察了电子商务发展与商品税收竞争强度之间的关系。主要发现如下:考虑到基于原产地的税收适用于实体店的购买,(i)基于目的地的电子商务税收竞争比基于原产地的税收竞争更激烈;(2)网络市场的扩张加剧了目的地税的竞争,同时缓解了原产地税的竞争。导致这一结果的主要因素是,当网上购物出现时,消费者将有一个新的选择,即“如何购买”,取代了“在哪里购买”的选择,而基于目的地的税收扭曲了后者的选择,而基于原产地的税收是中性的。

本文章由计算机程序翻译,如有差异,请以英文原文为准。

求助全文

约1分钟内获得全文

求助全文

来源期刊

International Tax and Public Finance

ECONOMICS-

CiteScore

2.40

自引率

10.00%

发文量

56

期刊介绍:

INTERNATIONAL TAX AND PUBLIC FINANCE publishes outstanding original research, both theoretical and empirical, in all areas of public economics. While the journal has a historical strength in open economy, international, and interjurisdictional issues, we actively encourage high-quality submissions from the breadth of public economics.The special Policy Watch section is designed to facilitate communication between the academic and public policy spheres. This section includes timely, policy-oriented discussions. The goal is to provide a two-way forum in which academic researchers gain insight into current policy priorities and policy-makers can access academic advances in a practical way. INTERNATIONAL TAX AND PUBLIC FINANCE is peer reviewed and published in one volume per year, consisting of six issues, one of which contains papers presented at the annual congress of the International Institute of Public Finance (refereed in the usual way). Officially cited as: Int Tax Public Finance

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: