Raslan Alzuabi, Sarah Brown, Mark N. Harris, Karl Taylor

{"title":"Modelling the composition of household portfolios: A latent class approach","authors":"Raslan Alzuabi, Sarah Brown, Mark N. Harris, Karl Taylor","doi":"10.1111/caje.12691","DOIUrl":null,"url":null,"abstract":"<p>We explore portfolio allocation in Great Britain by introducing a latent class modelling approach using household panel data based on a nationally representative sample of the population, namely the Wealth and Assets Survey. The latent class aspect of the model splits households into four groups, from lowest-wealth and least-diversified through to highest-wealth and most-diversified, which serves to unveil a more detailed picture of the determinants of portfolio diversification than existing econometric approaches. A pattern of class heterogeneity is revealed that conventional econometric models are unable to identify because the statistical significance and the direction of the effect of some explanatory variables vary across the groups. For example, the effect of labour income on the number of financial assets held influences the level of diversification for the two middle classes, whereas no effect is found for households with the lowest or the highest levels of diversification. Noticeable differences in the magnitude of the effects of pension wealth and occupation are also revealed across the four classes. Such findings demonstrate the importance of accounting for latent heterogeneity when modelling financial behaviour. Ultimately, treating the population as a single homogeneous group may lead to biased parameter estimates, whereby policy based on such models could be inappropriate or erroneous.</p>","PeriodicalId":47941,"journal":{"name":"Canadian Journal of Economics-Revue Canadienne D Economique","volume":"57 1","pages":"243-275"},"PeriodicalIF":1.3000,"publicationDate":"2023-10-26","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/caje.12691","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Canadian Journal of Economics-Revue Canadienne D Economique","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/caje.12691","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

Abstract

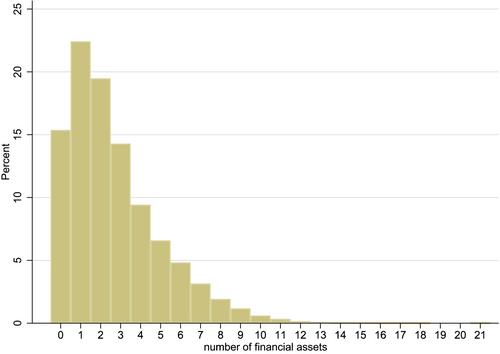

We explore portfolio allocation in Great Britain by introducing a latent class modelling approach using household panel data based on a nationally representative sample of the population, namely the Wealth and Assets Survey. The latent class aspect of the model splits households into four groups, from lowest-wealth and least-diversified through to highest-wealth and most-diversified, which serves to unveil a more detailed picture of the determinants of portfolio diversification than existing econometric approaches. A pattern of class heterogeneity is revealed that conventional econometric models are unable to identify because the statistical significance and the direction of the effect of some explanatory variables vary across the groups. For example, the effect of labour income on the number of financial assets held influences the level of diversification for the two middle classes, whereas no effect is found for households with the lowest or the highest levels of diversification. Noticeable differences in the magnitude of the effects of pension wealth and occupation are also revealed across the four classes. Such findings demonstrate the importance of accounting for latent heterogeneity when modelling financial behaviour. Ultimately, treating the population as a single homogeneous group may lead to biased parameter estimates, whereby policy based on such models could be inappropriate or erroneous.

期刊介绍:

The Canadian Journal of Economics (CJE) is the journal of the Canadian Economics Association (CEA) and is the primary academic economics journal based in Canada. The editors seek to maintain and enhance the position of the CJE as a major, internationally recognized journal and are very receptive to high-quality papers on any economics topic from any source. In addition, the editors recognize the Journal"s role as an important outlet for high-quality empirical papers about the Canadian economy and about Canadian policy issues.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: