{"title":"Advanced Displays, Materials Market Trends, and Unsettled Challenges","authors":"Kyle Jang, Bob O'Brien","doi":"10.1002/msid.1440","DOIUrl":null,"url":null,"abstract":"<p><b>SINCE THE INITIAL IMPLEMENTATION OF OLED DISPLAYS</b> on mobile phones in 2008, the OLED market has soared. In the annual market for smartphone displays (estimated at 1.3 billion units), OLED has secured approximately 50 percent market share and established itself as the leading technology in the smartphone display market.</p><p>But when OLED entered the premium TV market, while it gained attention, its growth was not as rapid as in the smartphone display market. This is because of ongoing technological improvements that address the limitations of LCD, resulting in a slower expansion of OLED within the premium TV market.</p><p>However, starting in 2022, Samsung Display's mass production of quantum dot OLED (QD-OLED) technology has renewed expectations for OLED's growth in the TV display market. Additionally, OLEDs, QD displays, and miniLEDs increasingly are being applied in IT devices and automotive displays, suggesting that competition between OLED and LCD will continue in the large- and medium-sized display markets.</p><p>The most prominent area for this competition is in the advanced TV market. In this field, consumers prioritize various display performance factors, such as resolution, power consumption, color reproduction, contrast ratio, and response time, as well as aspects such as size and thickness. Within the advanced TV market, LG Display's (LGD's) white OLED (WOLED) and LCD displays with QD technology, including QD-LCD and miniLED LCD, hold most of the market (<b>Fig</b>. 1). However, Samsung Display also introduced QD-OLED displays, adding a new dimension to the competition.</p><p>Display Supply Chain Consultants (DSCC) estimated the advanced TV market would be around 22 million units in 2022, with an expected compound annual growth rate (CAGR) from 2022 to 2027 of approximately 7.2 percent, growing to about 28 million units by 2025 and 30 million units by 2027.</p><p>OLED technology in TVs can be divided into WOLED (produced by LGD) and QD-OLED (produced by Samsung Display). Combined, these technologies are expected to maintain a market share of about 30 percent in the advanced TV market until 2027. QD display includes miniLED LCD, QD LCD, and QD-OLED; even excluding QD-OLED, it is expected to occupy ∼69 percent of the advanced TV market by 2027. QD-OLED is a technology that applies a QD color-conversion layer (QDCC) to blue OLED, falling into both OLED and QD-display categories.</p><p>The TV market is a core application of the flat panel display (FPD) industry, accounting for ∼70 percent of the total FPD area. Additionally, in the IT market (which includes monitors, notebook PCs, and tablets), although the quantity is smaller compared to smartphones, it holds a share of approximately 20 percent in terms of area within the FPD market. The smartphone display area accounts for less than 10 percent of the total FPD market.</p><p>Interestingly, QD and OLED display technologies are experiencing not only increased demand in advanced TVs, but also in IT and automotive displays. This suggests a positive outlook for aggressive growth in the OLED and QD display markets, provided that the underlying demand supporting this market growth continues.</p><p>In the display market, OLED evaporation and QD materials are critical to achieve high performance. OLED evaporation materials can be segmented into emitting layer materials and common materials. Emitting layer materials are the core materials that generate light in OLEDs, allowing for the representation of red, green, and blue (RGB). They consist of host and dopant materials and are the most important substances in OLED, directly impacting the brightness and lifespan of OLED displays.</p><p>Common materials are support materials used above and below the emitting layer. They have a vital function in facilitating the transport of electrons and holes generated at the cathode and anode into the emitting layer. Common materials enhance the stability of the OLED panel's emitting structure and support the efficiency improvement of emitting materials.</p><p>Research and development of OLED evaporation materials are carried out to optimize various factors, such as color accuracy and luminous efficiency. This is crucial for improving image quality and energy efficiency.</p><p>QD materials can be segmented into photoluminescent and electroluminescent (<b>Fig</b>. 2). Photoluminescent QD materials emit light when exposed to external light sources, such as the backlight unit (BLU). Film-type QDs used in LCD's BLU and QDCC materials used in OLEDs and microLEDs fall under this category. In the advanced TV market, QDCCs are applied in QD-OLED, whereas film-type QDs mainly are used in miniLED LCD and QD-LCD displays (Samsung, TCL, and others have designated these film-based QD-LCD TVs as “QLED”). These QD materials provide an expanded color gamut on screens, compensating for LCD's limited color expression compared to OLED.</p><p>Electroluminescent QD materials, known as QDEL, serve as substitutes for emitting materials in OLEDs. Similar to OLEDs, QDELs emit light on their own and are used to create RGB colors. QDELs are composed of inorganic materials and are considered a technology that can overcome OLED's main drawback—limited lifespan. They are one of the candidates for next-generation display technology.</p><p>OLED evaporation materials and QD materials are essential components in the display industry. When comparing the two markets, it is noteworthy that the OLED evaporation materials market is ∼15–20 times higher than that of QD materials.</p><p>In 2022, the OLED evaporation materials market was valued at ∼$1.3 billion, and it is projected to grow at a CAGR of ∼10 percent from 2022 to 2027, reaching ∼$2.2 billion by 2027 (see <b>Fig</b>. 3). Within this market, common layer materials are expected to account for ∼$744 million (roughly 34 percent), whereas emitting layer materials are projected to reach $1.4 billion (66 percent). When broken down by application, it is anticipated that by 2027, mobile OLED will account for ∼$1.2 billion (constituting 56 percent), whereas TV and other large-screen applications will reach nearly $1 billion (44 percent).</p><p>Revenues for OLED evaporation materials are expected to experience continuous growth in line with the ongoing expansion of OLED displays. There is a more optimistic outlook for OLED materials’ growth in IT, automotive, and TV applications, where tandem stacks are used, compared to mobile applications that typically employ a single stack.</p><p>To sustain this growth, it is necessary to address OLED's major weaknesses: luminance and lifespan. Panel manufacturers and OLED material companies are approaching this issue in three ways.</p><p>The first is fluorescent blue replacement. Currently, OLED uses phosphorescent materials for red and green, but fluorescent materials for blue. Although there has been a continuous development of blue phosphorescent materials and they meet panel manufacturers’ specifications in terms of luminance, lifetime performance is yet to be proven. Universal Display Corporation is actively developing phosphorescent blue materials and expects to adopt them to panel makers in 2024. Kyulux in Japan and Noctiluca in Poland are actively developing thermally activated delay fluorescence (TADF) technology, but they have not achieved significant breakthroughs for blue emitters.</p><p>Second, in the last couple of years, there has been a 20–30 percent improvement in efficiency by using blue materials with deuterium substitution technology. LGD adopted a deuterium-substituted blue host for its WOLED TV in 2022 and announced that the device's lifetime improved by 34 percent.<span><sup>1</sup></span> However, deuterium oxide is more difficult and expensive to obtain because of international regulations, which makes these materials twice as expensive as conventional ones.</p><p>The third method involves building a new stack structure with multiple emitting layers. OLED TV displays use a stack structure with 3–4 emitting layers, whereas IT and automotive displays use a two-stack structure. Increasing the number of stacks leads to more evaporation processes and the use of more OLED evaporation materials, which increases the cost of panels. However, relative to single-stack configurations, multi-stack configurations (2–4 stacks) can increase the lifespan and efficiency of OLED displays.</p><p>To compensate for OLED's luminance and lifespan issues, various technologies—such as double cathode protection layer (CPL), cathode pattern technology, multilens array (MLA), and color on encapsulation (COE)—are being developed and applied. However, the most critical technologies are the three mentioned, especially efficient blue materials. In the future, the key issue in the OLED evaporation material market will be which blue material technology can lead the market.</p><p>The QD materials market is expected to revolve around QD film, which is applied to QD-LCD, and QDCC, which is used for QD-OLED (<b>Fig</b>. 4). It is anticipated that QD material revenues used for QD-OLED will rise to $31 million by 2027. However, the growth of QDCC for QD-OLED is slow because investment in SDC's QD-OLED is progressing conservatively. QD-LCD will continue to be a core market for QD materials, and revenues in QD-LCD are expected to increase to ∼$100 million by 2027.</p><p>QDs also have opportunities with QDEL technology. QDEL can address OLED's lifespan issue, but it has not moved beyond the development stage, making it unlikely to be mass-produced within the next five years. If QDEL becomes commercialized, the QD materials market may rival the OLED materials market, although it may take some time.</p><p>OLED evaporation materials have secured a large market with attractive growth prospects. However, as long as luminance and lifetime remain weaknesses, there is an opportunity for a transition to other next-generation displays with even higher performance, such as QDEL or microLED. Therefore, the development of efficient and long-lasting blue-emitting materials is expected to be a critical point for the continued expansion and sustainability of the OLED market.</p><p>To expand the QD materials market, QD products should not expand in the premium sector where OLED dominates, but in the mid-range sector to achieve economies of scale. Likewise, in the premium segment, it is necessary to continue developing QDEL while leading with QDCC and applying it to QD-OLED or microLED to pioneer the future market. If QDEL's early entry into the market is possible, rapid growth in the QD materials market also is feasible.</p><p>The future of OLED evaporation materials’ and QD materials’ markets depends not only on addressing current challenges, but also on panel makers’ display technology selection strategies. In South Korea, both SDC and LGD are expanding their presence beyond mobile OLED and TV OLED to include IT and automotive OLED, while Chinese panel companies are still in the process of developing TV OLED technology and focusing on mobile and IT OLED. Furthermore, LGD and SDC have chosen different OLED technologies—WOLED and QD-OLED, respectively—each with its own strengths and limitations. This presents an additional risk to market expansion. To broaden the market, it is crucial for multiple companies to develop the same technology and engage in the market, promoting competition and growth.</p><p>In the case of OLED displays for smartphones, SDC, LGD, and several Chinese companies (including BOE, Visionox, Tianma, and CSOT) have entered the market, achieving a nearly 50 percent market share through technological and price competition. However, there are concerns about the limitations on expansion for OLED in the TV market, where such conditions do not exist.</p><p>Another risk to the OLED materials market is that panel companies consistently are developing next-generation displays beyond OLED. One of the most notable among them is microLED, which is already in mass production for TVs and signage, with expectations of soon being used for watches. QDEL also is consistently showcased in exhibitions and papers by various panel companies, and Samsung is developing a new technology called QNED (quantum dot nanorod emitting diode).</p><p>Given the emergence and release of various display technologies in the market, the continuous growth of OLED evaporation materials or the possibility of transitioning to a leadership role in QD materials will be determined by the display technology selection strategies of panel companies and the resolution of issues by material manufacturers.</p>","PeriodicalId":52450,"journal":{"name":"Information Display","volume":"39 6","pages":"31-34"},"PeriodicalIF":0.0000,"publicationDate":"2023-11-14","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://sid.onlinelibrary.wiley.com/doi/epdf/10.1002/msid.1440","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Information Display","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/msid.1440","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q4","JCRName":"Engineering","Score":null,"Total":0}

引用次数: 0

Abstract

SINCE THE INITIAL IMPLEMENTATION OF OLED DISPLAYS on mobile phones in 2008, the OLED market has soared. In the annual market for smartphone displays (estimated at 1.3 billion units), OLED has secured approximately 50 percent market share and established itself as the leading technology in the smartphone display market.

But when OLED entered the premium TV market, while it gained attention, its growth was not as rapid as in the smartphone display market. This is because of ongoing technological improvements that address the limitations of LCD, resulting in a slower expansion of OLED within the premium TV market.

However, starting in 2022, Samsung Display's mass production of quantum dot OLED (QD-OLED) technology has renewed expectations for OLED's growth in the TV display market. Additionally, OLEDs, QD displays, and miniLEDs increasingly are being applied in IT devices and automotive displays, suggesting that competition between OLED and LCD will continue in the large- and medium-sized display markets.

The most prominent area for this competition is in the advanced TV market. In this field, consumers prioritize various display performance factors, such as resolution, power consumption, color reproduction, contrast ratio, and response time, as well as aspects such as size and thickness. Within the advanced TV market, LG Display's (LGD's) white OLED (WOLED) and LCD displays with QD technology, including QD-LCD and miniLED LCD, hold most of the market (Fig. 1). However, Samsung Display also introduced QD-OLED displays, adding a new dimension to the competition.

Display Supply Chain Consultants (DSCC) estimated the advanced TV market would be around 22 million units in 2022, with an expected compound annual growth rate (CAGR) from 2022 to 2027 of approximately 7.2 percent, growing to about 28 million units by 2025 and 30 million units by 2027.

OLED technology in TVs can be divided into WOLED (produced by LGD) and QD-OLED (produced by Samsung Display). Combined, these technologies are expected to maintain a market share of about 30 percent in the advanced TV market until 2027. QD display includes miniLED LCD, QD LCD, and QD-OLED; even excluding QD-OLED, it is expected to occupy ∼69 percent of the advanced TV market by 2027. QD-OLED is a technology that applies a QD color-conversion layer (QDCC) to blue OLED, falling into both OLED and QD-display categories.

The TV market is a core application of the flat panel display (FPD) industry, accounting for ∼70 percent of the total FPD area. Additionally, in the IT market (which includes monitors, notebook PCs, and tablets), although the quantity is smaller compared to smartphones, it holds a share of approximately 20 percent in terms of area within the FPD market. The smartphone display area accounts for less than 10 percent of the total FPD market.

Interestingly, QD and OLED display technologies are experiencing not only increased demand in advanced TVs, but also in IT and automotive displays. This suggests a positive outlook for aggressive growth in the OLED and QD display markets, provided that the underlying demand supporting this market growth continues.

In the display market, OLED evaporation and QD materials are critical to achieve high performance. OLED evaporation materials can be segmented into emitting layer materials and common materials. Emitting layer materials are the core materials that generate light in OLEDs, allowing for the representation of red, green, and blue (RGB). They consist of host and dopant materials and are the most important substances in OLED, directly impacting the brightness and lifespan of OLED displays.

Common materials are support materials used above and below the emitting layer. They have a vital function in facilitating the transport of electrons and holes generated at the cathode and anode into the emitting layer. Common materials enhance the stability of the OLED panel's emitting structure and support the efficiency improvement of emitting materials.

Research and development of OLED evaporation materials are carried out to optimize various factors, such as color accuracy and luminous efficiency. This is crucial for improving image quality and energy efficiency.

QD materials can be segmented into photoluminescent and electroluminescent (Fig. 2). Photoluminescent QD materials emit light when exposed to external light sources, such as the backlight unit (BLU). Film-type QDs used in LCD's BLU and QDCC materials used in OLEDs and microLEDs fall under this category. In the advanced TV market, QDCCs are applied in QD-OLED, whereas film-type QDs mainly are used in miniLED LCD and QD-LCD displays (Samsung, TCL, and others have designated these film-based QD-LCD TVs as “QLED”). These QD materials provide an expanded color gamut on screens, compensating for LCD's limited color expression compared to OLED.

Electroluminescent QD materials, known as QDEL, serve as substitutes for emitting materials in OLEDs. Similar to OLEDs, QDELs emit light on their own and are used to create RGB colors. QDELs are composed of inorganic materials and are considered a technology that can overcome OLED's main drawback—limited lifespan. They are one of the candidates for next-generation display technology.

OLED evaporation materials and QD materials are essential components in the display industry. When comparing the two markets, it is noteworthy that the OLED evaporation materials market is ∼15–20 times higher than that of QD materials.

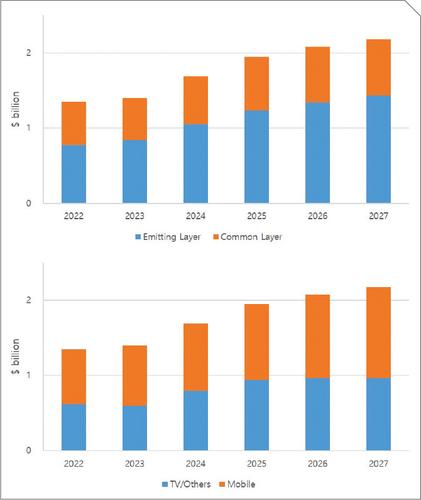

In 2022, the OLED evaporation materials market was valued at ∼$1.3 billion, and it is projected to grow at a CAGR of ∼10 percent from 2022 to 2027, reaching ∼$2.2 billion by 2027 (see Fig. 3). Within this market, common layer materials are expected to account for ∼$744 million (roughly 34 percent), whereas emitting layer materials are projected to reach $1.4 billion (66 percent). When broken down by application, it is anticipated that by 2027, mobile OLED will account for ∼$1.2 billion (constituting 56 percent), whereas TV and other large-screen applications will reach nearly $1 billion (44 percent).

Revenues for OLED evaporation materials are expected to experience continuous growth in line with the ongoing expansion of OLED displays. There is a more optimistic outlook for OLED materials’ growth in IT, automotive, and TV applications, where tandem stacks are used, compared to mobile applications that typically employ a single stack.

To sustain this growth, it is necessary to address OLED's major weaknesses: luminance and lifespan. Panel manufacturers and OLED material companies are approaching this issue in three ways.

The first is fluorescent blue replacement. Currently, OLED uses phosphorescent materials for red and green, but fluorescent materials for blue. Although there has been a continuous development of blue phosphorescent materials and they meet panel manufacturers’ specifications in terms of luminance, lifetime performance is yet to be proven. Universal Display Corporation is actively developing phosphorescent blue materials and expects to adopt them to panel makers in 2024. Kyulux in Japan and Noctiluca in Poland are actively developing thermally activated delay fluorescence (TADF) technology, but they have not achieved significant breakthroughs for blue emitters.

Second, in the last couple of years, there has been a 20–30 percent improvement in efficiency by using blue materials with deuterium substitution technology. LGD adopted a deuterium-substituted blue host for its WOLED TV in 2022 and announced that the device's lifetime improved by 34 percent.1 However, deuterium oxide is more difficult and expensive to obtain because of international regulations, which makes these materials twice as expensive as conventional ones.

The third method involves building a new stack structure with multiple emitting layers. OLED TV displays use a stack structure with 3–4 emitting layers, whereas IT and automotive displays use a two-stack structure. Increasing the number of stacks leads to more evaporation processes and the use of more OLED evaporation materials, which increases the cost of panels. However, relative to single-stack configurations, multi-stack configurations (2–4 stacks) can increase the lifespan and efficiency of OLED displays.

To compensate for OLED's luminance and lifespan issues, various technologies—such as double cathode protection layer (CPL), cathode pattern technology, multilens array (MLA), and color on encapsulation (COE)—are being developed and applied. However, the most critical technologies are the three mentioned, especially efficient blue materials. In the future, the key issue in the OLED evaporation material market will be which blue material technology can lead the market.

The QD materials market is expected to revolve around QD film, which is applied to QD-LCD, and QDCC, which is used for QD-OLED (Fig. 4). It is anticipated that QD material revenues used for QD-OLED will rise to $31 million by 2027. However, the growth of QDCC for QD-OLED is slow because investment in SDC's QD-OLED is progressing conservatively. QD-LCD will continue to be a core market for QD materials, and revenues in QD-LCD are expected to increase to ∼$100 million by 2027.

QDs also have opportunities with QDEL technology. QDEL can address OLED's lifespan issue, but it has not moved beyond the development stage, making it unlikely to be mass-produced within the next five years. If QDEL becomes commercialized, the QD materials market may rival the OLED materials market, although it may take some time.

OLED evaporation materials have secured a large market with attractive growth prospects. However, as long as luminance and lifetime remain weaknesses, there is an opportunity for a transition to other next-generation displays with even higher performance, such as QDEL or microLED. Therefore, the development of efficient and long-lasting blue-emitting materials is expected to be a critical point for the continued expansion and sustainability of the OLED market.

To expand the QD materials market, QD products should not expand in the premium sector where OLED dominates, but in the mid-range sector to achieve economies of scale. Likewise, in the premium segment, it is necessary to continue developing QDEL while leading with QDCC and applying it to QD-OLED or microLED to pioneer the future market. If QDEL's early entry into the market is possible, rapid growth in the QD materials market also is feasible.

The future of OLED evaporation materials’ and QD materials’ markets depends not only on addressing current challenges, but also on panel makers’ display technology selection strategies. In South Korea, both SDC and LGD are expanding their presence beyond mobile OLED and TV OLED to include IT and automotive OLED, while Chinese panel companies are still in the process of developing TV OLED technology and focusing on mobile and IT OLED. Furthermore, LGD and SDC have chosen different OLED technologies—WOLED and QD-OLED, respectively—each with its own strengths and limitations. This presents an additional risk to market expansion. To broaden the market, it is crucial for multiple companies to develop the same technology and engage in the market, promoting competition and growth.

In the case of OLED displays for smartphones, SDC, LGD, and several Chinese companies (including BOE, Visionox, Tianma, and CSOT) have entered the market, achieving a nearly 50 percent market share through technological and price competition. However, there are concerns about the limitations on expansion for OLED in the TV market, where such conditions do not exist.

Another risk to the OLED materials market is that panel companies consistently are developing next-generation displays beyond OLED. One of the most notable among them is microLED, which is already in mass production for TVs and signage, with expectations of soon being used for watches. QDEL also is consistently showcased in exhibitions and papers by various panel companies, and Samsung is developing a new technology called QNED (quantum dot nanorod emitting diode).

Given the emergence and release of various display technologies in the market, the continuous growth of OLED evaporation materials or the possibility of transitioning to a leadership role in QD materials will be determined by the display technology selection strategies of panel companies and the resolution of issues by material manufacturers.

期刊介绍:

Information Display Magazine invites other opinions on editorials or other subjects from members of the international display community. We welcome your comments and suggestions.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: