{"title":"Clustering-enhanced stock price prediction using deep learning.","authors":"Man Li, Ye Zhu, Yuxin Shen, Maia Angelova","doi":"10.1007/s11280-021-01003-0","DOIUrl":null,"url":null,"abstract":"<p><p>In recent years, artificial intelligence technologies have been successfully applied in time series prediction and analytic tasks. At the same time, a lot of attention has been paid to financial time series prediction, which targets the development of novel deep learning models or optimize the forecasting results. To optimize the accuracy of stock price prediction, in this paper, we propose a clustering-enhanced deep learning framework to predict stock prices with three matured deep learning forecasting models, such as Long Short-Term Memory (LSTM), Recurrent Neural Network (RNN) and Gated Recurrent Unit (GRU). The proposed framework considers the clustering as the forecasting pre-processing, which can improve the quality of the training models. To achieve the effective clustering, we propose a new similarity measure, called Logistic Weighted Dynamic Time Warping (LWDTW), by extending a Weighted Dynamic Time Warping (WDTW) method to capture the relative importance of return observations when calculating distance matrices. Especially, based on the empirical distributions of stock returns, the cost weight function of WDTW is modified with logistic probability density distribution function. In addition, we further implement the clustering-based forecasting framework with the above three deep learning models. Finally, extensive experiments on daily US stock price data sets show that our framework has achieved excellent forecasting performance with overall best results for the combination of Logistic WDTW clustering and LSTM model using 5 different evaluation metrics.</p>","PeriodicalId":49356,"journal":{"name":"World Wide Web-Internet and Web Information Systems","volume":"26 1","pages":"207-232"},"PeriodicalIF":3.4000,"publicationDate":"2023-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC9009501/pdf/","citationCount":"6","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"World Wide Web-Internet and Web Information Systems","FirstCategoryId":"94","ListUrlMain":"https://doi.org/10.1007/s11280-021-01003-0","RegionNum":3,"RegionCategory":"计算机科学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"COMPUTER SCIENCE, INFORMATION SYSTEMS","Score":null,"Total":0}

引用次数: 6

Abstract

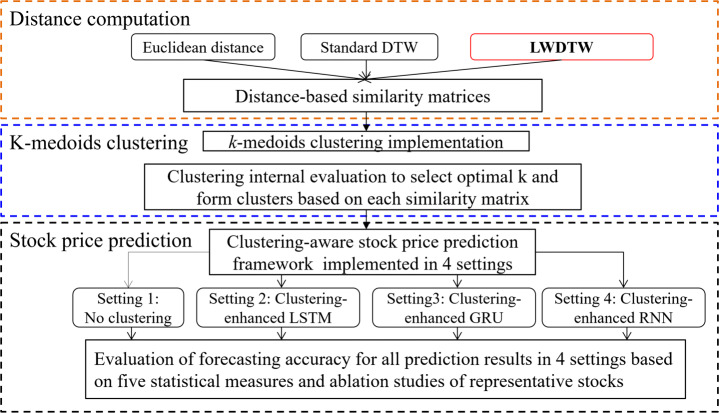

In recent years, artificial intelligence technologies have been successfully applied in time series prediction and analytic tasks. At the same time, a lot of attention has been paid to financial time series prediction, which targets the development of novel deep learning models or optimize the forecasting results. To optimize the accuracy of stock price prediction, in this paper, we propose a clustering-enhanced deep learning framework to predict stock prices with three matured deep learning forecasting models, such as Long Short-Term Memory (LSTM), Recurrent Neural Network (RNN) and Gated Recurrent Unit (GRU). The proposed framework considers the clustering as the forecasting pre-processing, which can improve the quality of the training models. To achieve the effective clustering, we propose a new similarity measure, called Logistic Weighted Dynamic Time Warping (LWDTW), by extending a Weighted Dynamic Time Warping (WDTW) method to capture the relative importance of return observations when calculating distance matrices. Especially, based on the empirical distributions of stock returns, the cost weight function of WDTW is modified with logistic probability density distribution function. In addition, we further implement the clustering-based forecasting framework with the above three deep learning models. Finally, extensive experiments on daily US stock price data sets show that our framework has achieved excellent forecasting performance with overall best results for the combination of Logistic WDTW clustering and LSTM model using 5 different evaluation metrics.

期刊介绍:

World Wide Web: Internet and Web Information Systems (WWW) is an international, archival, peer-reviewed journal which covers all aspects of the World Wide Web, including issues related to architectures, applications, Internet and Web information systems, and communities. The purpose of this journal is to provide an international forum for researchers, professionals, and industrial practitioners to share their rapidly developing knowledge and report on new advances in Internet and web-based systems. The journal also focuses on all database- and information-system topics that relate to the Internet and the Web, particularly on ways to model, design, develop, integrate, and manage these systems.

Appearing quarterly, the journal publishes (1) papers describing original ideas and new results, (2) vision papers, (3) reviews of important techniques in related areas, (4) innovative application papers, and (5) progress reports on major international research projects. Papers published in the WWW journal deal with subjects directly or indirectly related to the World Wide Web. The WWW journal provides timely, in-depth coverage of the most recent developments in the World Wide Web discipline to enable anyone involved to keep up-to-date with this dynamically changing technology.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: