Mahayaudin M. Mansor, David A. Green, Andrew V. Metcalfe

{"title":"Directionality and volatility in high-frequency time series","authors":"Mahayaudin M. Mansor, David A. Green, Andrew V. Metcalfe","doi":"10.1002/hf2.10008","DOIUrl":null,"url":null,"abstract":"<p>We provide empirical evidence of directionality in high-frequency multivariate time series of the five largest U.S. banks between 1999 and 2017. The directionality is more apparent during crisis periods than during noncrisis periods, and it has only a low association with volatility. We use directionality and volatility as a regime-switching criterion between two-regime threshold vector autoregressive (TVAR) models for forecasting share prices. We compare the forecasting performances using mean relative error squared, and a weighted average of the forecasting error, with weights based on the estimated conditional variance, for individual model components and as a group. We have demonstrated that moving directionality can provide early warning of increased volatility and crisis periods, and has potential for improving one-step ahead forecasts using TVAR(1) models.</p>","PeriodicalId":100604,"journal":{"name":"High Frequency","volume":"1 2","pages":"70-86"},"PeriodicalIF":0.0000,"publicationDate":"2018-01-19","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://sci-hub-pdf.com/10.1002/hf2.10008","citationCount":"2","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"High Frequency","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/hf2.10008","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"","JCRName":"","Score":null,"Total":0}

引用次数: 2

Abstract

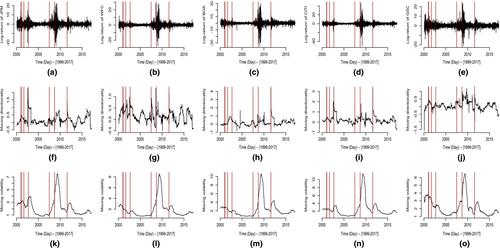

We provide empirical evidence of directionality in high-frequency multivariate time series of the five largest U.S. banks between 1999 and 2017. The directionality is more apparent during crisis periods than during noncrisis periods, and it has only a low association with volatility. We use directionality and volatility as a regime-switching criterion between two-regime threshold vector autoregressive (TVAR) models for forecasting share prices. We compare the forecasting performances using mean relative error squared, and a weighted average of the forecasting error, with weights based on the estimated conditional variance, for individual model components and as a group. We have demonstrated that moving directionality can provide early warning of increased volatility and crisis periods, and has potential for improving one-step ahead forecasts using TVAR(1) models.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: