Monitoring parameter change for bivariate time series models of counts.

IF 0.8

4区 数学

Q4 STATISTICS & PROBABILITY

引用次数: 0

Abstract

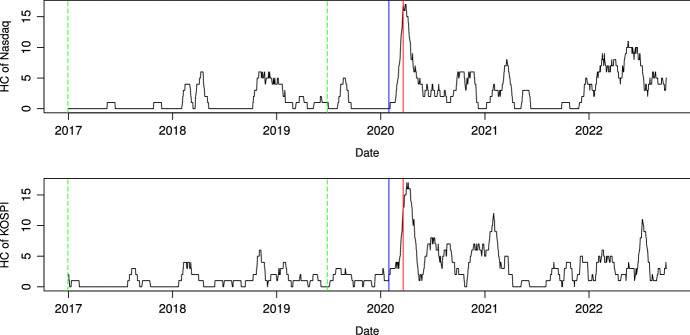

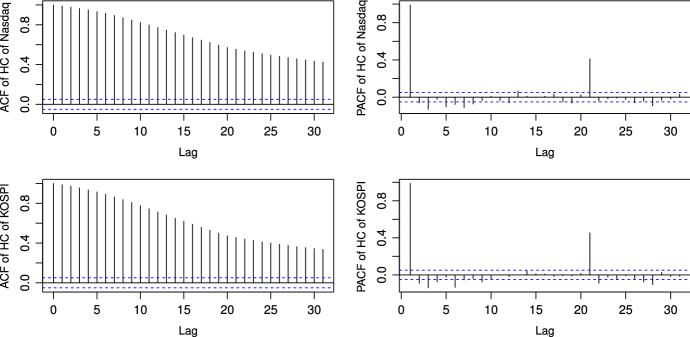

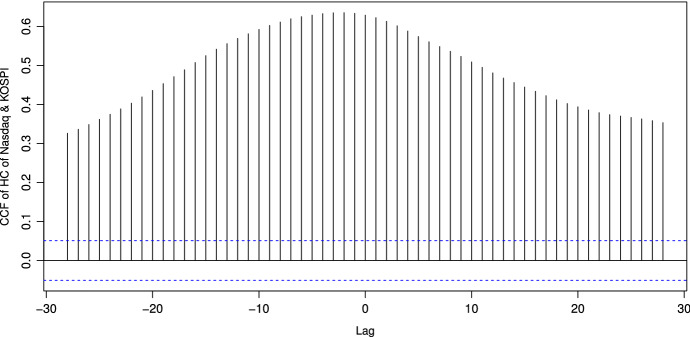

In this study, we consider an online monitoring procedure to detect a parameter change for bivariate time series of counts, following bivariate integer-valued generalized autoregressive heteroscedastic (BIGARCH) and autoregressive (BINAR) models. To handle this problem, we employ the cumulative sum (CUSUM) process constructed from the (standardized) residuals obtained from those models. To attain control limits, we develop limit theorems for the proposed monitoring process. A simulation study and real data analysis are conducted to affirm the validity of the proposed method.

监测计数的双变量时间序列模型的参数变化。

在本研究中,我们考虑了一种在线监测程序,以检测计数的二变量时间序列的参数变化,遵循二变量整数值广义自回归异方差(BIGARCH)和自回归(BINAR)模型。为了处理这个问题,我们使用累积和(CUSUM)过程,该过程是由从这些模型中获得的(标准化)残差构建的。为了达到控制极限,我们为所提出的监测过程发展了极限定理。通过仿真研究和实际数据分析,验证了该方法的有效性。

本文章由计算机程序翻译,如有差异,请以英文原文为准。

求助全文

约1分钟内获得全文

求助全文

来源期刊

Journal of the Korean Statistical Society

数学-统计学与概率论

CiteScore

1.30

自引率

0.00%

发文量

37

审稿时长

3 months

期刊介绍:

The Journal of the Korean Statistical Society publishes research articles that make original contributions to the theory and methodology of statistics and probability. It also welcomes papers on innovative applications of statistical methodology, as well as papers that give an overview of current topic of statistical research with judgements about promising directions for future work. The journal welcomes contributions from all countries.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: